The commercial and industrial solar market is broad – from a few panels on a storage facility, to a 500 acre solar power facility built to feed a Colorado steel mill, to the largest solar facilities in the world signing virtual power purchase agreements (PPA) to offset electricity usage hundreds of miles away.

Big solar PPAs get the best pricing, while onsite and “small” solar agreements get the best value. In 2015/2016, the installed volume of the two types of solar were roughly the same. Since then, onsite solar has doubled – while offsite virtual PPAs have grown 6X.

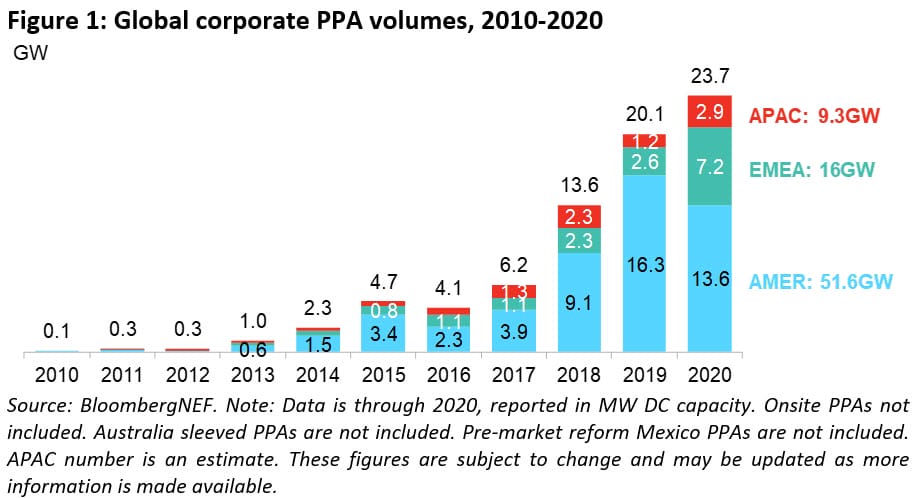

Bloomberg New Energy Finance reported that corporations purchased 23.7 GW of clean energy in 2020, up from 20.1 in 2019 and 13.6 in 2018. The USA led globally with 11.9 GW – even after declining from almost 14 GW in 2019. That growth globally occured, while the US shrank, shows the strength of the gathering storm.

In the USA, 2020 was the first time since the peak of 2016 that corporate purchasing declined. This contraction in signed contracts coincided with a near doubling of deployments in the USA in 2020.

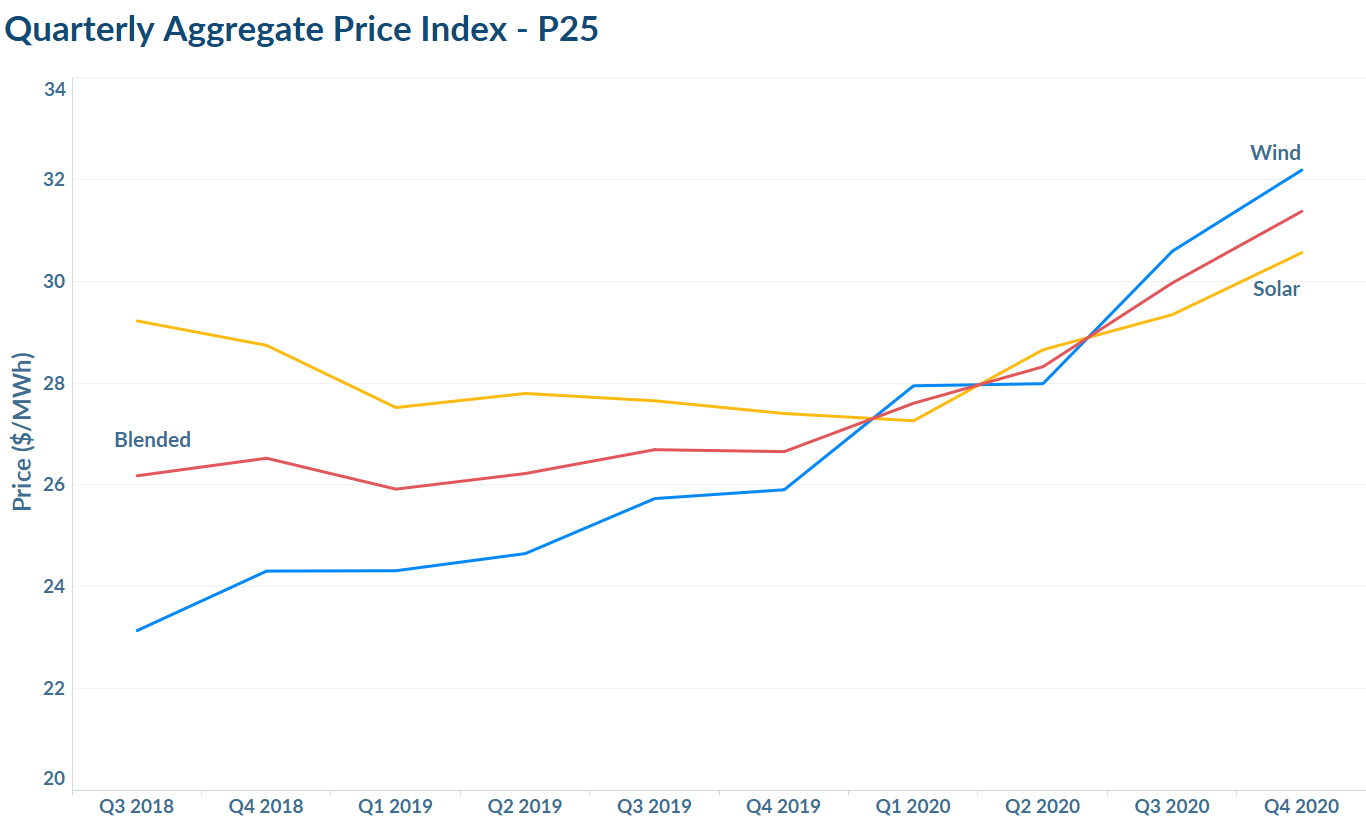

Three years of quarterly price index reports from LevelTen indicate that virtual solar PPAs have slowly, consistently declined due to falling costs, while wind PPAs have slowly, consistently risen as a result of Production Tax Credits phasing out. Starting in Q1 2020, solar PPA prices began rising, and wind PPA price increases rose more sharply, surpassing solar prices by 5.3%.

Grid connection delays and permitting challenges were cited as the top two factors impeding development in regions with high demand. Specifically, rising permitting and interconnection costs have been creating bottlenecks and upward pricing pressure. Demand to repower wind projects due to limited new power line capacity is growing as well.

Level Ten predicts further price increases in 2021, but wind and solar are still expected to remain the most economical form of electricity in the United States.

On NextEra’s Q4 earnings call, the nation’s largest solar power company (currently seeking to deploy 14.4 GWac solar+6.7 GW energy storage before 2024) was questioned by investors about its own C&I business. In Florida, via the NextEra subsidiary FPL, the company offers customers a chance to apply solar credits to their accounts from solar facilities already being built. This represents the company’s very centralized form of community’ish solar.

More interesting than that, is NextEra’s behind-the-meter 12 MW solar+hydrogen+fuel cell peaking power plant.

Peaking solar-hydrogen planthttps://t.co/NMwRiy7eL3 pic.twitter.com/iTjodbw9u1

— Commercial Solar Guy (@SolarInMASS) February 1, 2021

This is a beautiful collection of technology that could transition into an industrial use like steel, glass, or fertilizer production.

NextEra said they have multiple offerings working for C&I customers, and that the solar+hydrogen hardware is part of this suite of technologies. The company noted that their data collection and analysis expertise pairs well with the full suite of technologies – HVAC, batteries, transportation, and EV controls – that large C&I customers are seeking to refine.

All of those offerings combined with a peak plant and onsite generation demonstrate that NextEra has entered into the microgrid resilience business. It’s a good business to be in.

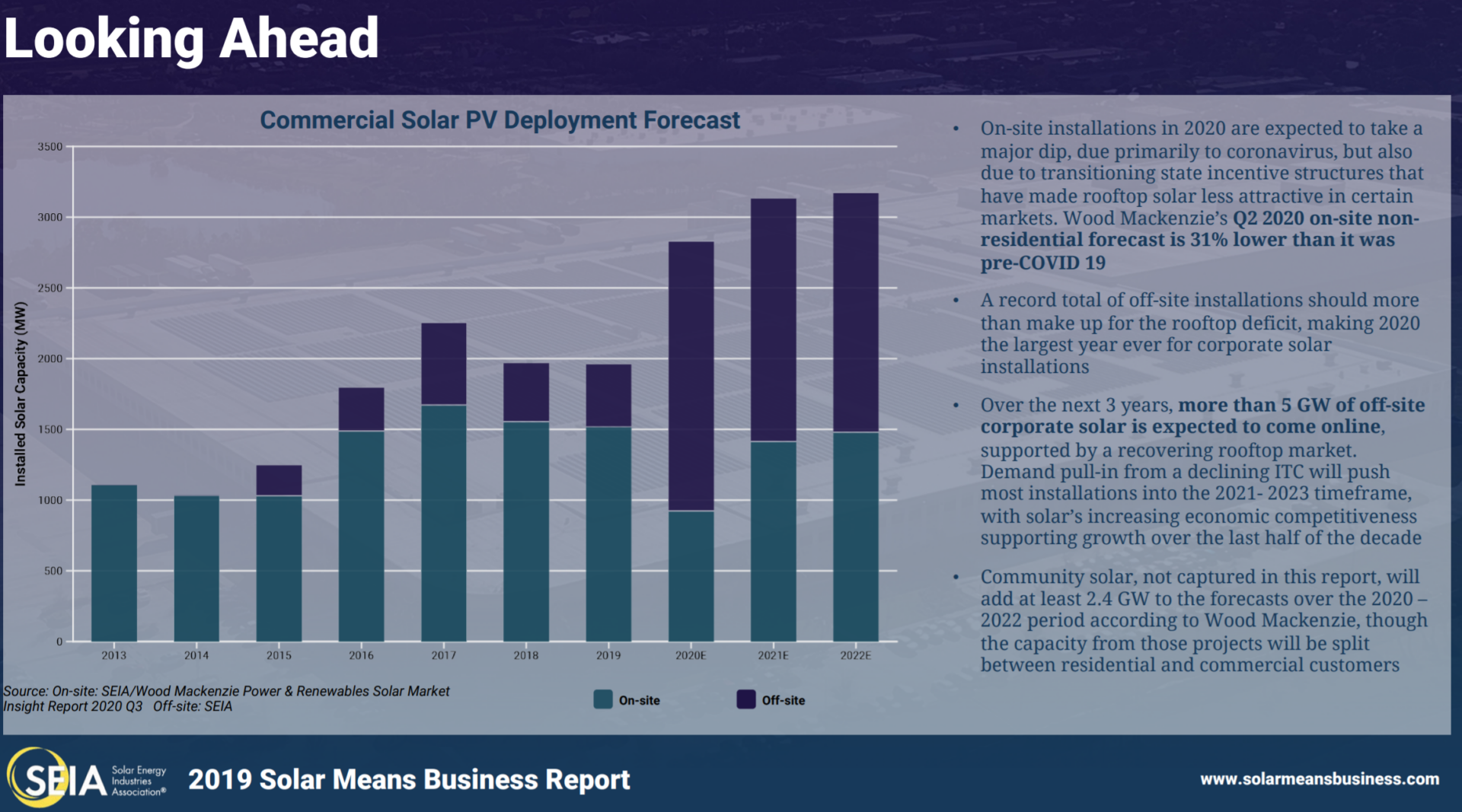

SEIA’s Solar Means Business report found that onsite commercial solar installation volume has actually fallen since 2015 through the end of 2020. At a minimum, this is because of the growth of the utility scale PPAs noted by BNEF/Level Ten above. It is also partially a result of events such as Walmart needing to sue Tesla as a result of regular fires due to badly chosen components in the company’s solar projects.

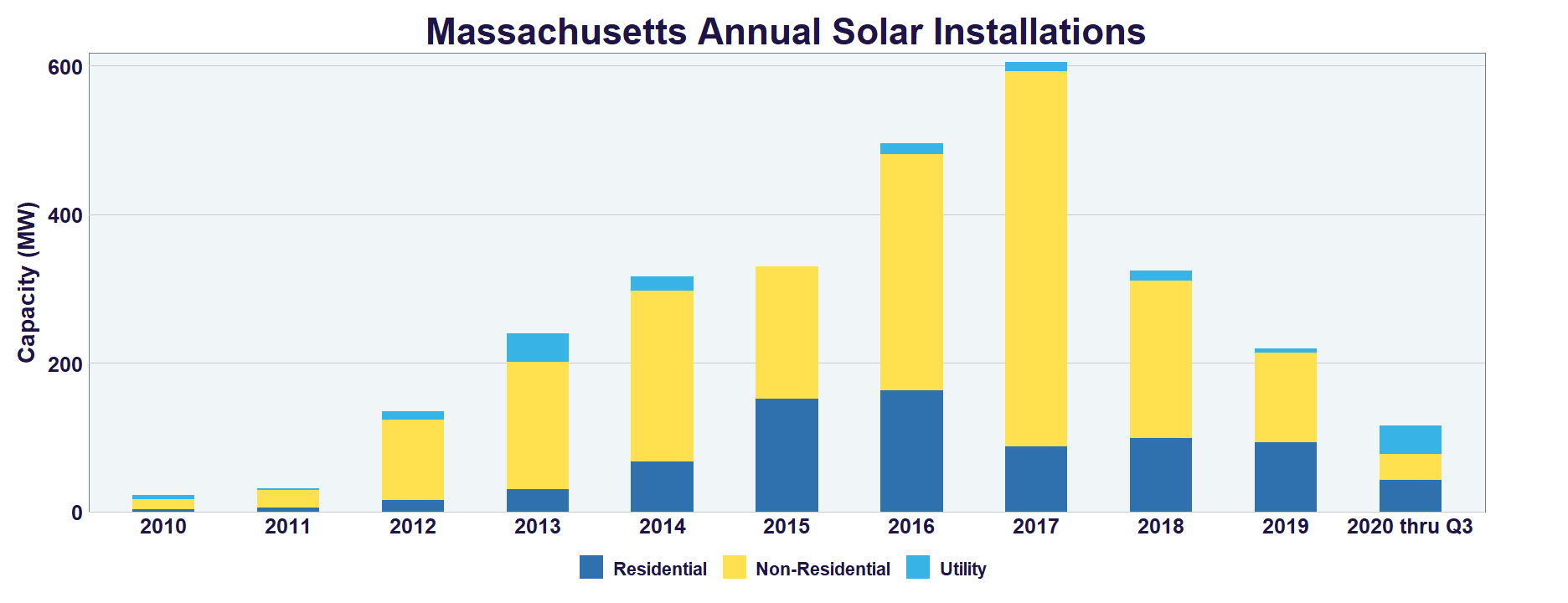

In key C&I markets of the United States, like Massachusetts, the volume deployed has waxed and – over the past few years – waned, as incentive programs have come and gone and interconnection queues expanded.

Though, do expect the tides to turn again, because law and the mighty dollar will pull rooftop solar by the nose.

The California residential rooftop solar power mandate will soon expand to all governments and commercial structures. Massachusetts’ most recent climate legislation contains a backdoor residential rooftop requirement.

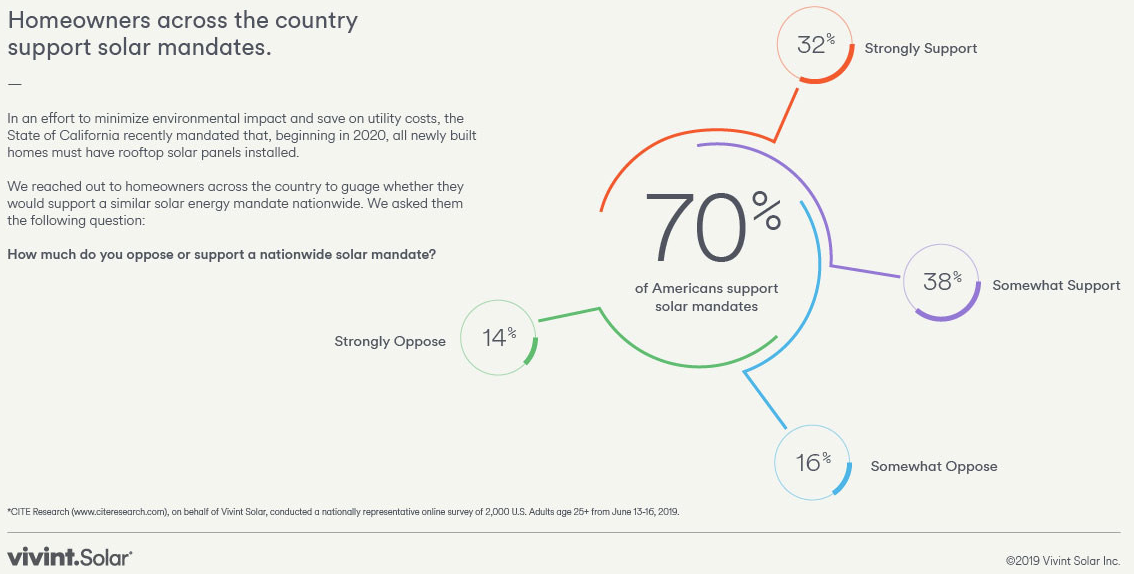

CITE Research finds that America strongly supports a rooftop solar mandate – 70% of America in fact. Former Vivint CEO David Bywater noted, …’with nearly a million new single-family homes built annually, if all of them took advantage of solar energy, it would be equivalent to driving 12 billion fewer miles a year.’

In truth, the support for rooftop commercial solar will come from the local value it provides. There are hundreds of billions on the table – in the form of savings on electricity bills. And multiples more in dollars earned by those who install this capital and labor intensive, distributed resource.

https://twitter.com/PhilippLitz/status/1350746726093770752

Yes, it will cost more, however global solar-political markets show that public support tends to follow a wide distribution of revenue from solar+storage.

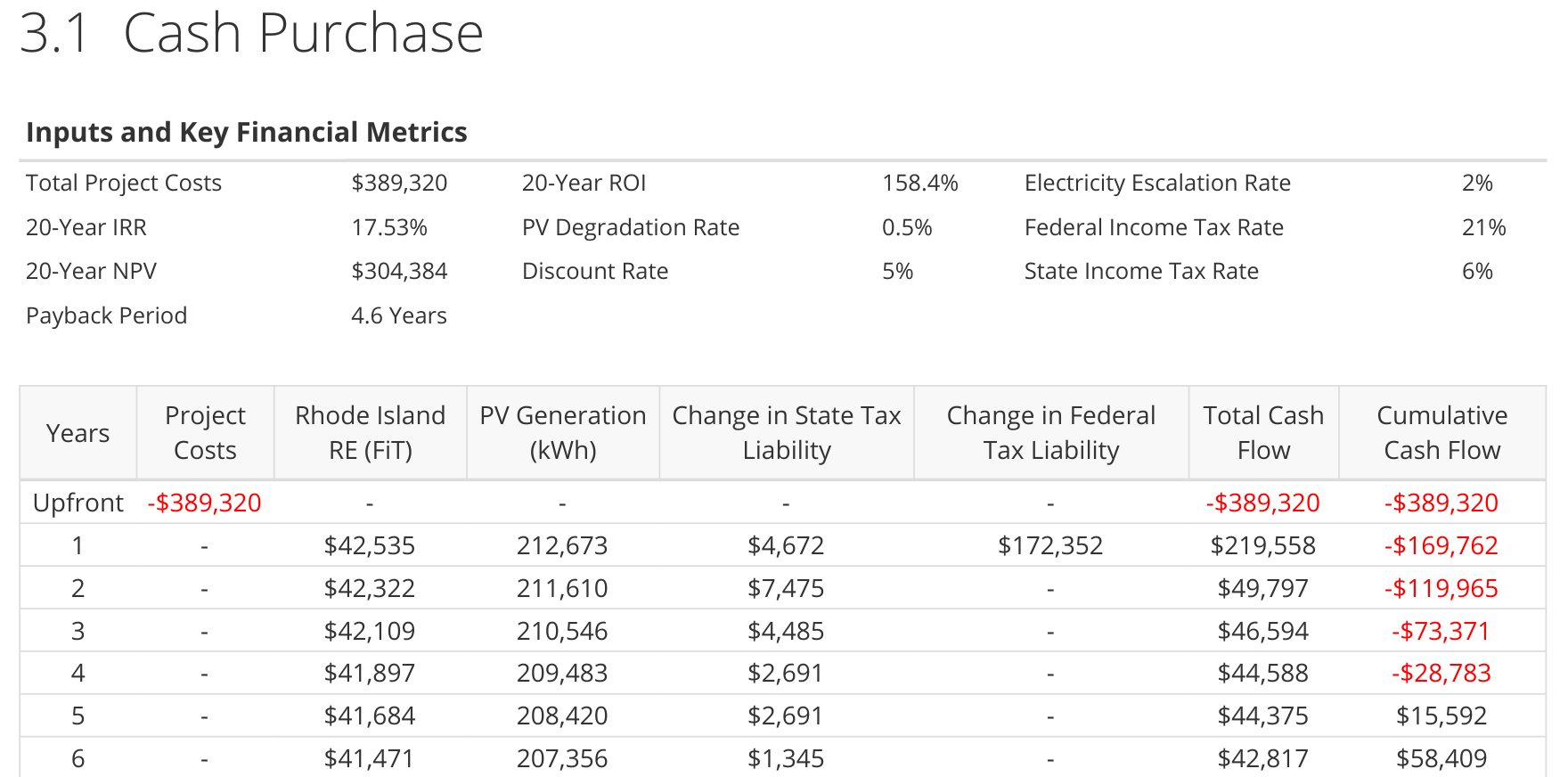

CommercialSolarGuy specifically installs rooftop systems of high value. A recent installation of ours in Rhode Island gave the building owner a payback under five years. The project employed a team of three installers and an electrician for a month and half.

While the price per watt of this installation was twice that of a large scale ground mount, there is significant local value to the business owner (above), its neighbors, and the installers.